As the Trump Presidency begins, anxieties linger about cuts in government spending, stock market uncertainty, and even some fears of a recession. But since interest rates fall during a recession, it could actually be good news for the home-buying market in 2017. A whole new generation of previous renters will become first-time homeowners. Easy home expense calculators, online resources, and apps like FeeBelly are the tech-savvy millennial's way of avoiding hidden fees when buying a house.

As the Trump Presidency begins, anxieties linger about cuts in government spending, stock market uncertainty, and even some fears of a recession. But since interest rates fall during a recession, it could actually be good news for the home-buying market in 2017. A whole new generation of previous renters will become first-time homeowners. Easy home expense calculators, online resources, and apps like FeeBelly are the tech-savvy millennial's way of avoiding hidden fees when buying a house.

All the fees associated with buying a house can be quite daunting for first-timers. Buying a new home involves a lot of people, and at the closing, unexpected costs will add up. Even routine and legal fees, though more visible today that in the past, can hide behind other prioritized costs. There are so many fees to understand, that even if they're not in the fine print, they can be overlooked. Aside from principal mortgage and interest costs, and of course real estate commission, there are a few other big expenses.

Common, yet easily overlooked, & hidden fees when buying a house:

- Origination fees - These include the cost of pulling your credit report, underwriting and document preparation fees, and other administrative costs.

- Home and pest inspection, appraisal and survey fees - These can add up to several hundred dollars, but could save you much more in the future.

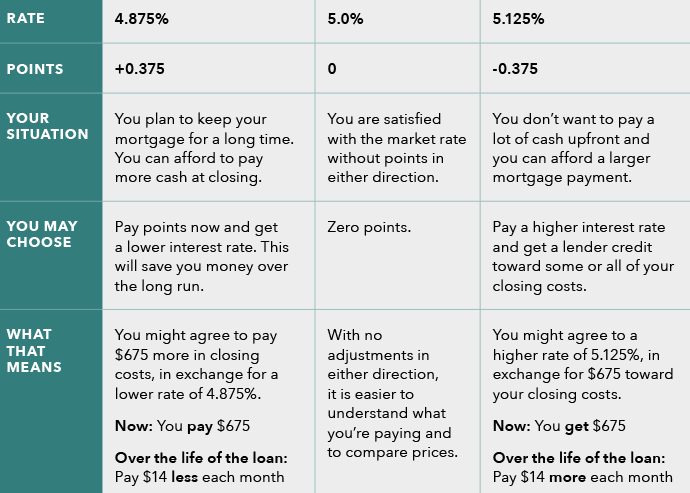

- Points - Seemingly foreign to some new home buyers, points are a percentage of the loan. Lenders offer different interest rates with different loans.

- Title fees - There are more of these fees than you might imagine. They include a title insurance binder, lender and owner title insurance, and title search fees.

- Tax fees - Property and homeowner’s tax are fairly well-known, but watch out for a transfer tax too.

- Insurance fees - The most understood fees are home warranty and homeowner's insurance. Less so is private mortgage insurance, or PMI. If your down payment is less than 205% you'll also have this PMI fee. In earthquake or high flood zones, you'll need extra insurance too. And you'll even pay a flood determination fee to decide if you need to pay extra!

- Escrow Fees - This can be another unfamiliar process to new homebuyers, but you might be required to pay some of your property taxes and insurance into an escrow account upfront.

- HOA or condo fees - Homes within a homeowners' association (HOA) or a condominium association will require a monthly or quarterly fee.

- Other miscellaneous fees - Notary, recording, and settlement and attorney fees may also apply, and can vary from state to state.

{kind=link}

New Age Preparation

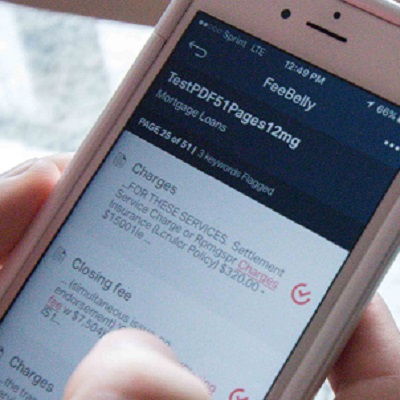

Some of the costs outlined are required up front, and some can be rolled into your home loan. The fees can also vary by state and circumstance. Hundreds of factors can contribute to which hidden fees when buying a house should concern you. So, do yourself a huge favor and check into the details of each of these fees thoroughly. Ask for a Good Faith estimate, which outlines your closing costs in detail. Do some research on your own (don't just trust the lender or agent). And get yourself a fine print detective for finding hidden fees - all you have to do is upload a PDF or scan your documents with your phone. For the millennial generation, buying a new home is ‘huuuuge!’, and it's a fact technology and online resources can help.